“Know what you own, and know why you own it”

“Understand the nature of the companies you own and the specific reasons for holding the stock. (“It is really going up!” doesn’t count.)”

What do you think is Nestle’s main product?

Maggi?

Nescafe?

Munch?

Kitkat?

While most of these products are visible to the consumer eye and have been consumed by most of us on multiple occasions, what people often tend to miss are their category leading — money making — monopoly brands.

Mind you: me, you, my parents and your parents and probably our children — all have had / will have exposure to this product.

Cerelac, Lactogen & NAN

This video by Sonjoy Bhattacharya will give you a great perspective on how powerful the brands Lactogen, Cerelac and NAN are and why they will continue to be monopolies in the future, unless of course some new player comes and disrupts it (Similac from Abbott looks like the nearest competitor — but more on that later).

YouTube Link: Investing with Sanjoy Bhattacharya

In case you do not wish to watch the video / haven’t watched it, the relevant synopsis is — No mother is going to experiment with her new born baby in trying a new brand for Infant Food or cereal — that is the kind of MOAT — Competitive Advantage that Nestle enjoys for multiple years and will continue to do so.

I have almost had this verified by so many people from so many different income groups — and I have gotten more confirmation than contradiction on this fact.

Let’s look at Nestle’s Investor Presentation

Market Share of their brands

Source: Investor Presentation, Q2FY19

96% value share in the Infant Cereal Market — Let that sink in for a while.

A simple Google search will tell you the number of babies born in India in a day, let’s take a conservative estimate and say that 10% of that number buys Cerelac / Lactogen and NAN and extrapolate that number.

Compare that with the sales of Nestle over the last 10 years — you should have your answer.

Let’s also have a look at the Revenue mix of all the brands (category — wise) that Nestle has.

When Maggi got banned in the country, the stock had corrected from 7,000 to 5,700/5,400 levels — making it one of the most attractive times to enter. While this may be regarded as a Black Swan event that may / may not happen again, it may have given someone who bought at that level tremendous boasting rights to have had bought the stock then to say today that the stock is now trading at 15,000 levels.

While there was no change that happened to the remaining 70% of the revenue mix, it was a fraction of the 30% category of the Company that had got affected (as can be seen from the image above).

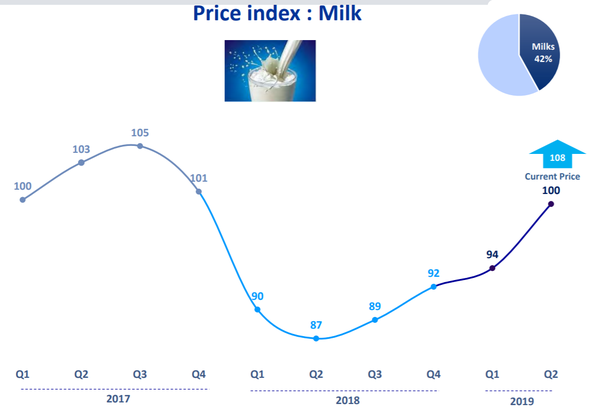

Now, while we have talked about the Revenue side, let’s take a focus on the cost side. Most of the raw material cost that Nestle incurs is on Milk (~42%) as per their Investor Presentation.

The Indian milk market has been a really tough nut to crack. Various companies have tried and failed multiple models in this country. The fact that the global diary major Danone came to India and went back should speak volumes about how sourcing milk in India is not an easy game.

So much so that when we think of milk only two names pop in our head — Amul and Nestle. While we all know what Amul has done in this country and continues to do so, (GCMMF — Gujarat Co — Operative Milk Marketing Federation is the entity behind Amul), GCMMF is not listed and hence a lot of data is not available in the public domain. This brings us to the closest nation wide listed player — Nestle.

Until recently we have seen a flurry of startups trying to “disrupt” the milk market, along with a host of other established FMCG companies getting into dairy. Who will survive and who will flourish — only time will tell. As I write this article and have 200 other tabs open in my browser, it is disheartening to read that Doodhwala (a dairy based startup) has shut shop.

Coming back to Nestle.

Power packed Brands — Check

Market Leaders in categories that it operates in — Check

Sourcing Strength — Check

Nestle’s numbers have been phenomenal and ticks all the boxes of what Saurabh Mukherjea calls to be a “Classic Compounder” making it a great company. It’s Return on Capital Empoyed (dhandha’s return) has been consistently higher than 50% going to even 130–140% in some years for decades. The company has planned multiple launches for the future and is presently focusing on giving more extensions to its existing brands.

Anytime it makes over and above what it does — which it does most of the times, it gives it as special dividend — over and above their regular dividend. They had recently announced a special dividend of 200 in the month of August.

Just to give you some perspective, I use the Maggi masala sachet on almost everything from chips to egg whites and what not. It was launched at a price of 3 then 4 and now it’s at 5 within almost a year (pricing power).

I have seen various street food vendors use the masala on almost anything and everything that they sell.

Nescafe Chilled Latte was a product that was long overdue and we can see how that is being consumed all round the year now.

How can we forget our beloved Maggi?

It still has around 20–30 launches planned for 2019

Should you buy the Nestle stock?

In a nutshell, identify great companies and invest in them — don’t have a trader’s mentality of shortchanging yourself saying — oh look, I bought at 100, exited at 150 only to realize the stock is now at 4,000 8 years later. Think of yourself as a part owner of the Company. Would you want to setup a factory, invest in brands, hire a sales team and fire them after 4 months?

The above article was originally published by Saket Mehrotra https://qr.ae/TJuSCd

If you liked this article, please do share share it (Whatsapp, Twitter) with other Traders/Investors.